June 12, 2024: Investment Strategies Amid AI Boom and Economic Uncertainty: The Impact of CPI, FOMC, and Dollar Strength

Simultaneous CPI and FOMC Announcements: “A Boring Meeting”?

As we approach the dual major events of the May Consumer Price Index (CPI) and the Federal Open Market Committee (FOMC) announcements tomorrow, investors are adopting a cautious stance. Wall Street Journal (WSJ) reporter Nick Timiraos has predicted, “If a disappointing inflation report comes out tomorrow morning, more Fed members could suggest a single rate cut this year.” He also added, “A report in line with expectations could lead more members to advocate for two rate cuts.” Such articles have heightened market vigilance.

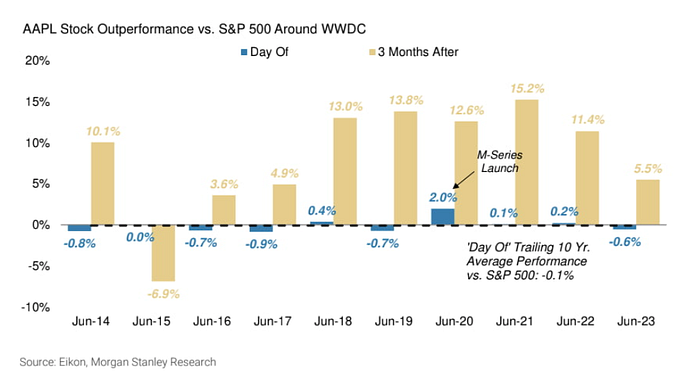

Apple’s AI Strategy and Stock Surge

Apple announced its AI strategy yesterday, achieving a record high in its stock price. The AI strategy focused on personalization and security enhancements, which received positive feedback from users. Wedbush analyst Dan Ives evaluated the announcement, stating, “Apple provided everything it needed.” The AI features are expected to drive the iPhone upgrade cycle, as highlighted during Apple’s Worldwide Developers Conference (WWDC). JP Morgan analyzed that “Apple’s WWDC was sufficient to bolster confidence in the expected upgrade cycle.”

JP Morgan further stated, “Apple’s WWDC provided enough assurance about the expected upgrade cycle. The stock might take a breather, but consumer surveys indicate that hardware replacement cycles are increasingly driven by feature upgrades. Overall, around 1.4 billion iPhones are expected to be upgraded in the coming years.”

Morgan Stanley noted, “The WWDC slightly exceeded our expectations. It featured key factors that could trigger device replacements over the next few years.”

DA Davidson expressed, “We believe the AI features unveiled at WWDC yesterday will drive the iPhone upgrade cycle. Just as digital music transitioned from standalone apps like Napster to consumer apps like iTunes, this integration (through AI) will significantly broaden AI adoption.”

Market Reaction and Economic Indicators

The S&P 500 index recorded an all-time high for the second day in a row despite the upcoming doubleheader. This surge is largely due to Apple’s stock price increase after unveiling its AI strategy and a sharp drop in rates as foreign investors flocked to the 10-year US Treasury auction in the afternoon.

JP Morgan’s Tyler Head analyzed that if the core CPI falls between 0.20% and 0.25% month-over-month, expectations for a rate cut in September could soar. Additionally, if it falls below 0.2%, the S&P 500 index could rise by 1.75–2.50%.

FOMC Outlook and Market Predictions

WSJ published an early morning article by Timiraos, known as the “unofficial spokesperson” of the Fed, predicting the FOMC’s actions. Key points include:

- The benchmark rate is expected to be maintained at 5.25–5.5%.

- The policy statement is likely to imply that the next move is more likely a cut than a hike.

- Focus will be on the so-called “dot plot” due to the expected lack of significant policy changes.

- The dot plot could be finalized at the last minute based on the CPI report due Wednesday morning.

- Many investors assume that two rate cut proposals are needed to lower rates by September.

UBS’s base case is for the dot plot to show two rate cuts. However, if tomorrow’s CPI exceeds expectations following strong May employment, more members might step back from rate cuts.

UBS stated, “The June FOMC will make decisions impacting the FOMC in July, September, and November. If most members propose a single 25bp cut this year, it’s unlikely enough data will emerge by then to reconsider a rate cut in July or September. Thus, suggesting one cut this year in the June meeting effectively closes the door on rate cuts until December.”

Franklin Templeton’s Ed Perks, CEO of Income Advisors, said, “The Fed will stay the course tomorrow. It’s likely to be a very dull meeting.” Bank of America also stated, “Neither the CPI nor the FOMC will be game-changers.”

Predictions indicate that CPI will be in line with expectations and that there will be no significant changes from the FOMC. Vital Knowledge founder Adam Crisafulli stated, “If the dot plot shows one or two rate cuts this year, that’s already priced into the market. Zero would be problematic because it means no rate cuts this year.”

Changes in the Bond Market and Investor Reactions

Yesterday in the New York bond market, the 10-year Treasury yield surged to 4.469% and maintained this level throughout the morning. However, the auction results announced at 1 PM significantly shifted market sentiment.

The auction’s issuance rate was set at 4.438%, 2bp below the market yield of 4.458% at the time of issuance. The bid-to-cover ratio was 2.67, well above the six-auction average of 2.50 and the highest since early 2022, before Fed tightening began. Indirect demand, reflecting foreign interest, was 74.5%, the highest since February 2023.

A bond market insider explained that the increased demand for long-term Treasuries ahead of the CPI announcement was due to growing political uncertainty in Europe, particularly in France, leading to a flight to US Treasuries.

Bookvar Report founder Peter Bookvar questioned, “Is the market smelling a soft CPI tomorrow, or is it concerned about economic growth slowing?” These factors caused the 10-year Treasury yield to drop by 6.7bp to 4.402% by 5 PM, and the 2-year yield fell by 5.1bp to 4.834%.

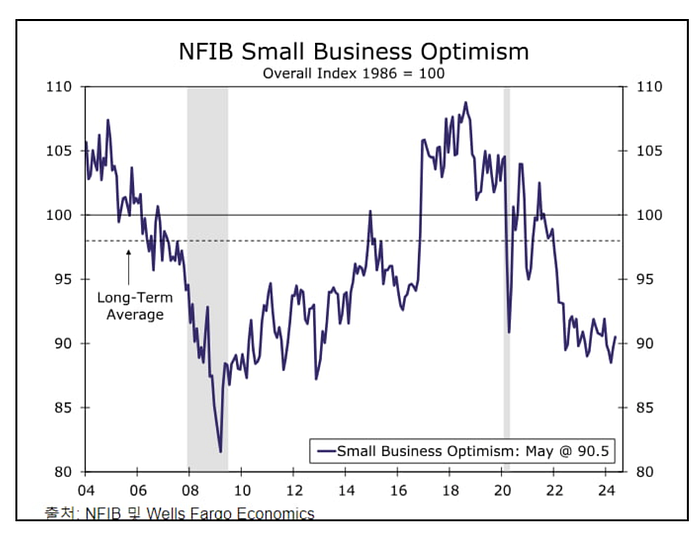

Small Business Optimism Index and Consumer Expectation Survey

The National Federation of Independent Business (NFIB) reported that the Small Business Optimism Index for May rose by 0.8 points to 90.5 from April, marking two consecutive months of increases. While this is the highest level this year, it still falls short of the 50-year average of 98. Given that bank loan rates for small businesses exceed 9%, the low level is understandable.

However, expectations for the business environment over the next six months have risen, showing the least negative outlook since August 2021. Although the percentage of businesses planning to increase employment is at 15%, the lowest since the early pandemic, this is a positive signal.

Additionally, the New York Federal Reserve’s May consumer expectation survey indicated an improvement in households’ current financial situations. The percentage of respondents expecting to be as well-off or better off financially in 12 months rose to 78.1%, the highest since June 2021. The percentage expecting higher stock prices in 12 months also rose by 1.8 points to 40.5%, the highest since May 2021.

Retail Sales and Economic Outlook

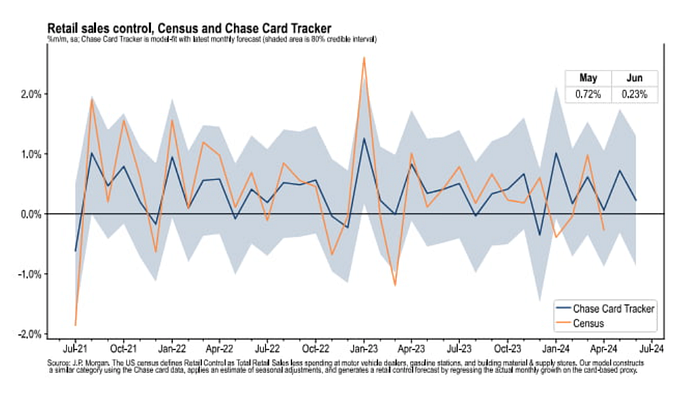

Johnson Redbook reported that May retail sales increased by 5.5% year-over-year. JP Morgan estimated that based on Chase credit card spending, retail sales in May surged by 0.72% from the previous month. Bank of America calculated the likelihood of a hard landing for the US economy at 10–15%, with a soft landing at 45–50% and no landing at 30–35%.

New York Stock Exchange and Major Corporate Earnings

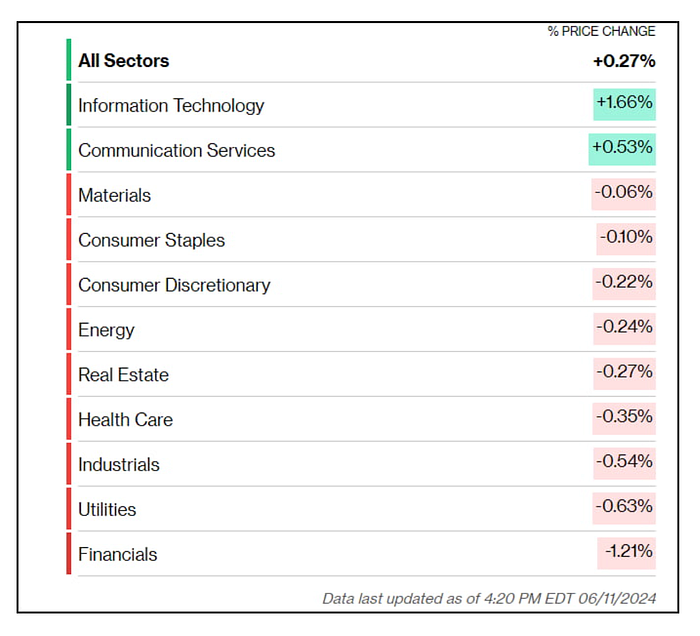

The major indices in the New York Stock Exchange opened with a 0.1–0.3% decline but turned positive as Apple surged and bond auction announcements led to a sharp drop in rates. The Nasdaq ultimately rose 0.88%, and the S&P 500 index increased by 0.27%. Only the Dow ended down by 0.31%.

Apple soared by 7.26% to reach $207, recording an all-time high for the first time this year. DA Davidson analyst Gil Luria analyzed, “Apple’s growth through AI could accelerate to low, mid, or even high single digits over the next 12 years.” This will be a significant factor moving Apple’s stock price.

Meanwhile, financial stocks plunged, with JP Morgan falling by 2.63%. This shock was triggered by the news that a commercial building in Manhattan, New York, was sold for $50 million, a 67% discount from its 2018 purchase price. PIMCO warned, “We expect more regional bank failures as commercial real estate loans are heavily concentrated on some balance sheets.”

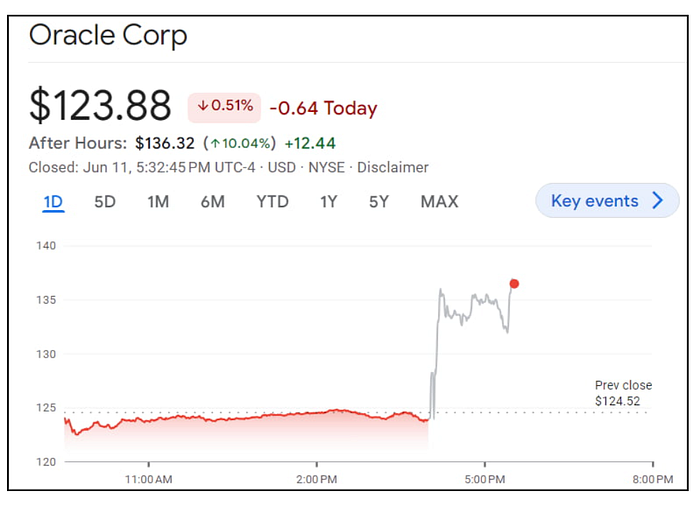

Oracle Earnings Announcement

Oracle’s Q4 earnings, announced after market close, fell short of expectations. Adjusted EPS was $1.63, missing the expected $1.65, and revenue was $14.29 billion, below the expected $14.55 billion. However, the stock surged 10% in after-hours trading, thanks to the AI boom. Oracle announced it would provide its database to Google starting November and that OpenAI had chosen Oracle’s cloud for additional computing capacity.

AI Boom and Market Concentration

The recent AI boom has raised concerns that stock price increases are concentrated in AI and big tech stocks. According to Bespoke Investment, the six stocks in the S&P 500 with market caps over $1 trillion rose by 11.5% in Q2, while the remaining 494 stocks fell by an average of 3%. This concentration is primarily driven by the AI boom, with the S&P 500 index hitting all-time highs, but only 4% of stocks actually reached new highs. Such a concentrated market is expected to eventually see reduced concentration due to mean reversion.

Richard Bernstein’s Deputy CIO Dan Suzuki argued, “The greatest risks are where capital is crowded and concentrated. That’s very true now. There has never been a time with higher concentration than today.” While the upward trend in stock prices continues, high concentration could persist for quite some time. John Hancock Investment strategist Matt Miskin explained, “The market has never been this concentrated. However, the concentration could deepen further.”

Focus on High-Quality Stocks

Morgan Stanley CIO Mike Wilson advises focusing on high-quality stocks in such a concentrated market. He has partially turned away from pessimism but has not fully adopted an aggressive stance. Wilson analyzed, “Over the past few months, data has increasingly fallen short of growth expectations, and inflation has been skewed upward.” He emphasized, “This means the Fed is in a complicated situation where it still cannot cut rates.”

Wilson advised, “High rates are putting pressure on many parts of the economy and consumption, eventually reflecting poor performance in small caps. Invest in high-quality assets.” He argued that the stock price surge in lower-quality assets would be impossible until the Fed makes significant rate cuts. He stressed that meaningful cuts would require dropping rates by at least several hundred basis points.

Dollar Strength and Economic Outlook

Dollar strength is also negatively impacting the market. Following political instability in Europe, particularly in France, the dollar has continued to strengthen, with the euro-dollar exchange rate falling to $1.073 today from $1.09. The ICE Dollar Index rose by 0.11% to 105.26.

Goldman Sachs predicts that the dollar will retain most of its recent gains this year. “The strength of the US economy” is the main reason, with the economy showing resilience despite high interest rates, and future Fed rate cuts unlikely to significantly erode the dollar’s value. Better growth or higher asset yields in other regions of the world could lead to dollar depreciation, but scenarios like the US presidential election could strengthen the dollar.

Morgan Stanley also argued, “Predictions of dollar depreciation might be significantly exaggerated.” They suggested that while the dollar could weaken if the Fed continues to cut rates, its dominant status as a reserve currency would keep its value strong. They also pointed to factors such as central banks’ holdings of dollar assets and its role in global trade and finance as sustaining the dollar’s dominance.