June 4, 2024: Economic Slowdown and Wall Street’s Sensitive Response: Trends in Bond and Stock Markets

Economic Slowdown and Wall Street’s Sensitive Response

Despite several positive events over the weekend, the New York Stock Exchange started strong on Monday morning (Eastern Time). This was due to a sharp drop in oil prices and falling interest rates. However, when the Institute for Supply Management (ISM) economic data was released and turned out worse than expected, interest rates fell significantly, and market anxiety began to spread. Are we now at a point where an economic slowdown is no longer perceived as just “bad news”?

OPEC+ Production Cuts and Falling Oil Prices

At the OPEC+ meeting on June 2, an agreement was reached to extend production cuts of 3.66 million barrels per day until the end of 2025. This decision was due to the lack of strong demand growth. However, key players like Saudi Arabia and Russia, among others, agreed to extend additional voluntary cuts of 2.2 million barrels per day until September this year, gradually reducing them from October to September next year.

In essence, while the cuts are extended in name, actual production will gradually increase. Additionally, the UAE was allowed to increase its production from 2.9 million barrels per day to 3.5 million barrels next year.

Javier Blas, an energy columnist at Bloomberg Economics, stated, “OPEC+ production will increase by more than 500,000 barrels per day by December and by approximately 1.8 million barrels by mid-2025. OPEC+ had been aiming for $100 per barrel, but they have now given up on almost everything.”

July West Texas Intermediate (WTI) crude fell 3.60% to close at $74.22 per barrel, the lowest level since February 7. Brent crude also fell 3.4% to $78.36 per barrel, the lowest since February 5. The drop in oil prices was a major factor in the decline in interest rates. As oil prices plummeted, the decline in interest rates became more pronounced.

The Economic Relationship Between Oil Production Cuts and Interest Rate Declines

Oil is a crucial raw material for economic activities, and oil prices affect various economic costs. When oil prices rise, transportation and production costs, among other expenses, increase, leading to higher consumer prices. Conversely, when oil prices fall, these costs decrease, leading to lower inflation.

Central banks, such as the U.S. Federal Reserve (Fed), use interest rate policies to control inflation. When inflation rises, central banks may raise interest rates to curb economic activity and lower inflation. Conversely, when inflation falls, central banks may lower interest rates to stimulate economic activity.

Production Cuts and Oil Prices

When major oil-producing countries, such as those in OPEC+, cut oil production, the reduced supply typically leads to higher oil prices. However, in recent situations, oil prices have sometimes fallen despite OPEC+ production cuts. This can occur if the scale of the cuts does not meet market expectations or if demand remains weak.

Falling Oil Prices and Economic Expectations

When oil prices fall, expectations for lower inflation increase. This can be interpreted as a signal that central banks will have less need to raise interest rates. Consequently, markets may anticipate a decline in interest rates, and in many cases, interest rates actually fall.

Bond Market Reaction

As expectations for lower inflation increase with falling oil prices, the bond market often anticipates a decline in interest rates, leading to rising bond prices. When interest rates fall, the value of existing bonds rises relative to new issues, increasing bond purchasing activity. This results in a decrease in bond yields (interest rates).

The Future of AI Chips and Tech Stock Strength

At the Computex event in Taiwan on June 2, Nvidia and AMD announced that they would accelerate the product cycle of AI chips. Nvidia CEO Jensen Huang declared that new AI chip models would be launched on an “annual basis,” with the Blackwell model coming out later this year, the Blackwell Ultra in 2025, and the Rubin platform in 2026.

Bank of America raised its target price for Nvidia to $1,500, stating that it “strengthens Nvidia’s AI leadership position.” AMD CEO Lisa Su also announced plans to enhance the AI chip MI300 series with the Instinct MI325X series and to release the MI350 in 2025 and the MI400 series in 2026.

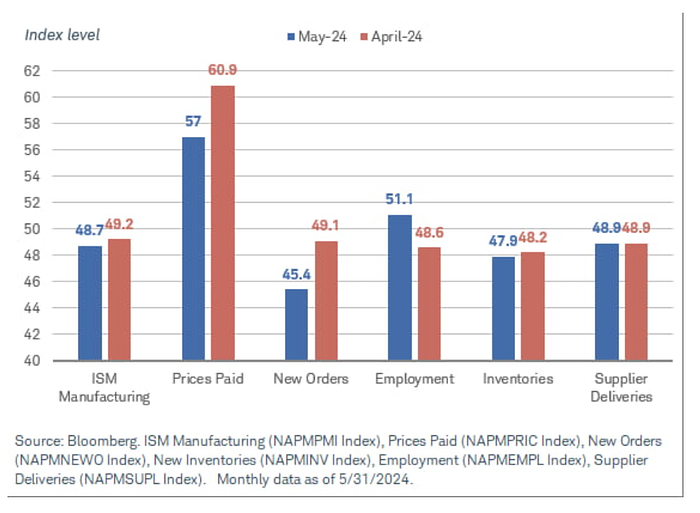

Manufacturing PMI and Economic Outlook

The ISM May Manufacturing PMI, released at 10 AM, recorded 48.7, down from 49.2 in April and below Wall Street’s expectation of 49.6. Notably, new orders fell sharply by 3.7 points to 45.4, and production declined to 50.2. However, employment increased by 2.5 points to 51.1, returning to expansion territory.

Corporate responses generally indicated an economic slowdown. A chemical company noted, “There seems to be a slight slowdown,” and a machinery company stated, “Orders are increasing, but new orders are not coming in.” An electrical equipment and appliance company mentioned, “Reservations for May and June are decreasing,” while a furniture company reported, “Business is recovering, and reservations are increasing.” ISM analysts commented, “Due to restrictive monetary policies, companies are hesitant to invest, making it difficult to gauge demand.”

BMO stated, “The ISM manufacturing index defied expectations for a slight improvement due to high interest rates and weak demand, indicating weak demand for goods.” Capital Economics added, “The May manufacturing PMI decline, with new orders at a 12-month low, suggests the economy is losing momentum. The drop in the prices paid index from 60.9 to 57.0 is also good news for the Fed.”

Allianz advisor Mohamed El-Erian remarked, “The ISM manufacturing PMI hit a three-month low in May. The sharp decline in new orders significantly contributed to the index drop. This data aligns with other signs that the economy is losing momentum.”

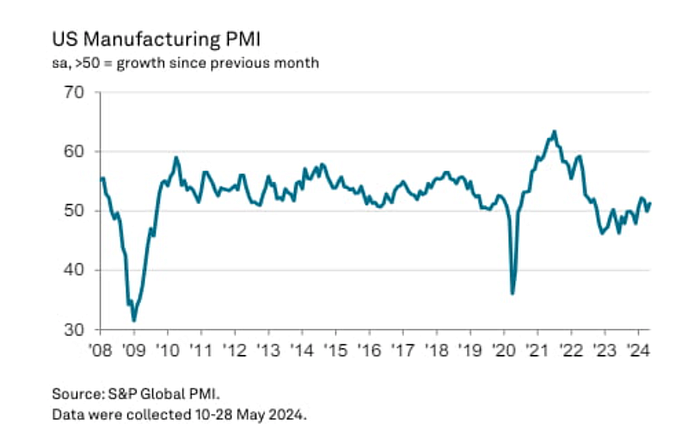

However, S&P Global’s May manufacturing PMI was 51.3, surpassing April’s 50.0. Ned Davis Research stated, “The contrasting May manufacturing PMIs from ISM and S&P Global highlight uncertainty about the actual state of manufacturing activity. The average of the two PMIs slightly rose to 50.0 in May.”

Decline in Construction Spending and Economic Outlook

The Commerce Department reported a 0.1% decrease in April construction spending compared to the previous month. Private spending fell 0.1%, while public spending increased 0.8%. ING analyzed, “The construction sector showed more weakness than expected, indicating that monetary policy is restraining economic activity.”

Wall Street’s Economic Recession Forecast

Signs of an economic slowdown have rekindled recession fears on Wall Street. Advisor Mohamed El-Erian stated, “The market consensus on the Fed remains hawkish, with many investors expecting a rate cut this year. This expectation aligns with the Fed’s data-dependence but not with the Fed’s own stance.”

Renaissance Macro economist Neil Dutta commented, “Current conditions are favorable, but it’s hard to argue they align with meaningful acceleration. The Fed remains highly uncertain.” He outlined four potential scenarios:

- Steady growth and slowing inflation (soft landing)

- Slowing growth and slowing inflation (soft landing)

- Slowing growth and accelerating inflation (stagflation)

- Recovery in growth and inflation, returning to boomflation

Dutta added, “I still think the risk of scenario 1) is higher than 2), but this now seems irrelevant. Therefore, I would now prefer bonds over stocks.”

Vital Knowledge noted, “The economy seems to be at a turning point. Headwinds are blowing, and things are slowing down. This will benefit bonds but send mixed signals for stocks.”

Bond Market Reaction and Stock Market Volatility

With the economic indicators cooling, there was a buying spree in the bond market. As of 5 PM, the 10-year U.S. Treasury yield plunged 12 basis points to 4.392%, and the 2-year yield fell 8.1 basis points to 4.812%. The sharp decline in interest rates caused some stock market investors to freeze. Consequently, the three major indices all briefly fell into negative territory.

Interactive Brokers strategist Jose Torres analyzed, “Bad news may no longer be good news. In recent months, investors have welcomed weak data on hopes it would accelerate the Fed’s easing, but now they are reacting with fear.”

Nvidia and Big Tech Stocks Rise

Nevertheless, Nvidia bolstered the New York Stock Exchange. Nvidia surged 4.89%, and TSMC rose 2.59% on the accelerated chip supply announcement by Nvidia and AMD. ARM jumped 5.48%, and Micron gained 2.54%. However, AMD erased its early gains and closed down 2.01%. ‘Safe haven’ Big Tech stocks also held up well, with Amazon up 1.08%, Apple 0.93%, and Meta 2.28%.

Ultimately, the Nasdaq rose 0.56%, the S&P 500 gained 0.11%, and the Dow fell 0.3%. Stocks other than Nvidia, semiconductors, and Big Tech were weak. Of the 11 S&P 500 sectors, four (IT, healthcare, communication services, and consumer discretionary) rose, while seven declined. The energy sector plummeted 2.60% amid the oil price collapse.

Divergence in Market Outlook

There are mixed outlooks for the market. Morgan Stanley CIO Mike Wilson believes the bull market will continue. He argued, “Increasing government debt will continue to stimulate fiscal spending, inflating asset prices, including stocks, as long as the bond market shows no signs of stress.”

Conversely, JPMorgan Global Research Head Marco Kolanovic stated, “Inflation deceleration and economic ‘no landing,’ and consensus disagreement on corporate earnings acceleration will limit market gains during the summer.”

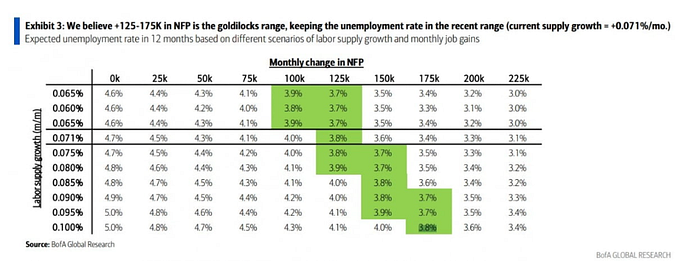

Bank of America’s Savita Subramanian and Kwon Oh-sung, who had previously advocated for a bullish stance, are now stepping back slightly. Subramanian said, “Extremely bearish sentiment is no longer a tailwind for the index, and we must focus on an active stock selection strategy.” Kwon Oh-sung added, “If growth deteriorates too much, bad news could turn into bad news, presenting a ‘Goldilocks’ range of 125,000 to 175,000 for monthly nonfarm payrolls. However, if it falls below 125,000, the trend of bad news being good news could reverse.”

Economic Slowdown and Unemployment Forecast

The Labor Department’s May nonfarm payroll report is scheduled to be released this Friday. Bank of America expects an increase of 200,000 jobs, with the unemployment rate remaining at 3.9%. The Wall Street consensus is for 185,000 jobs and a 3.9% unemployment rate.

Charles Schwab bond strategist Colin Martin stated, “The weaker-than-expected ISM report indicates that monetary policy is restrictive enough to slow economic activity and lower inflation. If the unemployment rate rises above 4%, it would mean the labor market is truly slowing, increasing the likelihood of a Fed rate cut this year.”