March 27, 2024 : A Sudden Shift from a Quiet Start in the Financial Markets: Analyzing the Trends of the New York Stock Exchange and the Mixed Economic Indicators

Financial Market Trends: A Quiet Start Followed by a Downturn

On March 26, 2023, Eastern Time in the United States, the New York financial markets were mostly quiet for the majority of the day. The economic data released did not significantly impact the market, with most big tech stocks maintaining their equilibrium.

However, as the market approached the last 30 minutes before closing, a surge of selling led to a downturn; the S&P 500 index fell by 0.28%, the Nasdaq by 0.42%, and the Dow Jones showed a slight underperformance with a 0.08% drop. This movement is attributed to investors adjusting their positions ahead of the Good Friday holiday and the upcoming February Personal Consumption Expenditures (PCE) price index announcement.

Key Corporate Stock Performance

- Apple experienced a 0.67% decrease in its stock price following reports of a 33% decrease in iPhone shipments in China compared to the previous year. However, the announcement of the upcoming Developers Conference (WWDC) scheduled for June 10–14 mitigated the decline.

- Tesla saw a 2.92% increase in its stock price despite Bernstein’s downward revision of its Q1 delivery estimates from 490,000 to 426,000 vehicles and a decrease in its target price from $150 to $120. The boost came after announcing a one-month free trial of its Full Self-Driving (FSD) software.

- Nvidia’s stock fell by 2.57% despite a significant increase in market value over 15 months, due to Bloomberg’s report on the uncertainty of demand and increasing competition.

‘Trump Stocks’ and the Meme Stock Surge

The newly NASDAQ-listed ‘Trump Media & Technology Group (TMTG)’ and meme-favorite Reddit experienced a surge in early trading hours but saw their gains significantly reduce by the market close. TMTG, founded by former President Donald Trump and parent company of ‘Truth Social’, rose by 16% on its first day of trading, even hitting a peak of 60%. Despite reporting a revenue of $3.4 million and a loss of $49 million in the first nine months of the previous year, and a 39% decrease in users, the company garnered attention. Steve Sosnick from Interactive Brokers likened owning TMTG stock to betting on Trump’s re-election possibilities through call options.

Mixed Economic Indicators

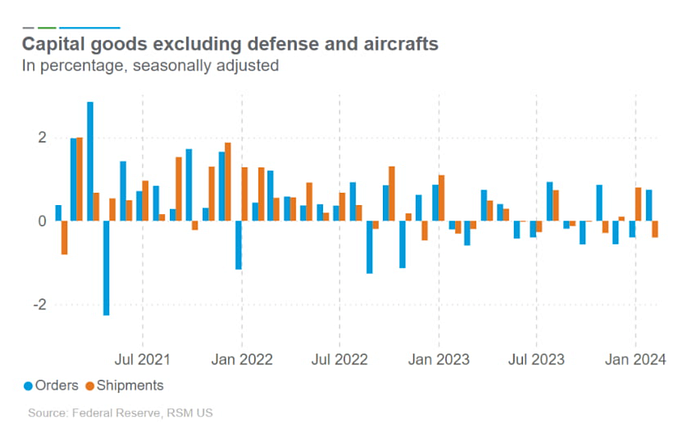

Today’s economic indicators presented a mixed view. February’s durable goods orders increased by 1.4% month-over-month, slightly above Wall Street’s expectation of a 1.3% rise.

However, this was set against a backdrop of a downward revision for January’s figures. The non-defense capital goods orders excluding aircraft, an indicator of business investment, turned positive, indicating potential for a manufacturing rebound. Capital Economics suggested that the recovery would continue, supported by falling corporate bond yields.

Consumer Confidence and Housing Prices

The Conference Board’s March consumer confidence index fell slightly to 104.7, below the anticipated 106.7, yet auto and home purchase intentions among consumers rose. Despite high gasoline prices pushing the 12-month inflation expectations from 5.2% to 5.3%, Wells Fargo noted that consumer confidence remained stable, with an improved outlook on the job market but growing pessimism about future income increases could pose challenges for spending. January’s housing prices showed a year-on-year increase of 6.6%, attributed to falling mortgage rates, though the month-over-month growth remained stable at 0.14%.

Regional Economic Indices and GDP Forecasts

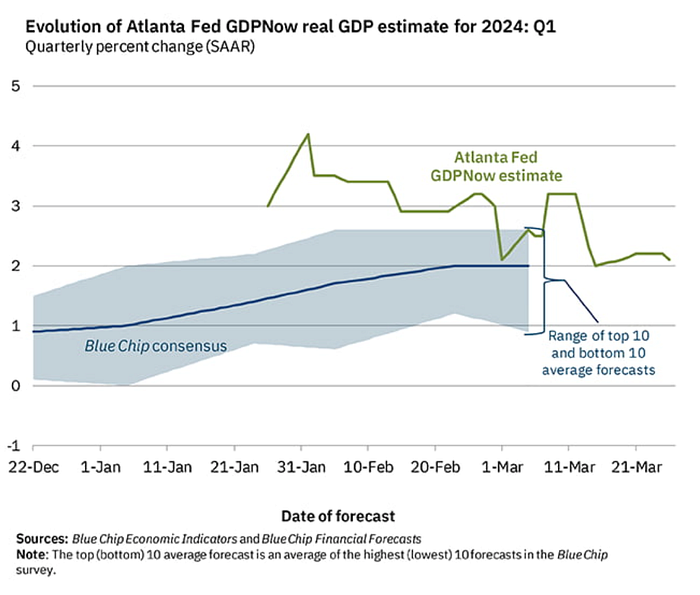

The service and manufacturing indices from the Philadelphia and Richmond Federal Banks underperformed expectations, leading Goldman Sachs to slightly lower its Q1 GDP growth forecast to 1.8%, while the Atlanta Federal Bank’s GDPNow maintained a 2.1% expectation.

Bond Market Trends and National Debt Concerns

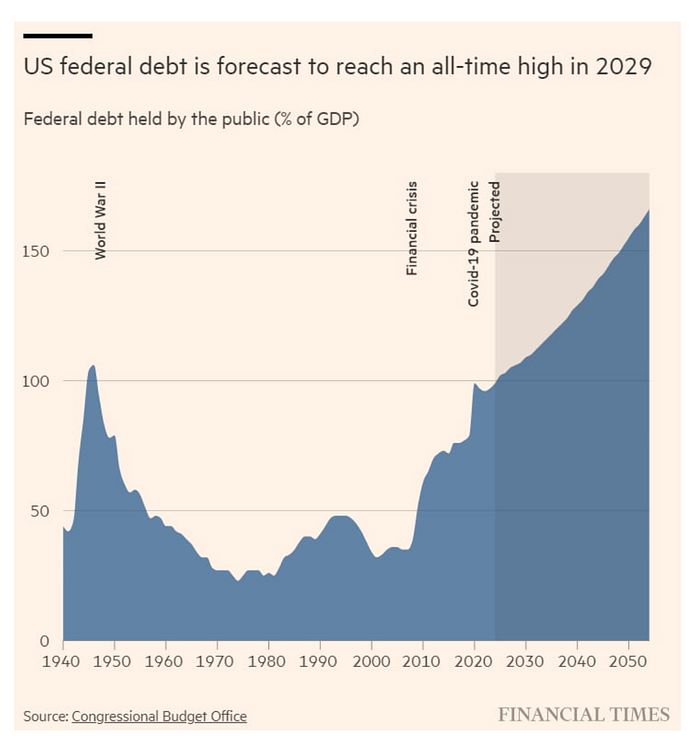

The New York bond market showed mixed signals with the 10-year Treasury yield slightly decreasing and the 2-year yield marginally increasing. The Financial Times reported concerns voiced by the U.S. Congressional Budget Office Director about the potential for a fiscal crisis similar to the one faced by former UK Prime Minister Liz Truss in 2022 if the burgeoning national debt is not addressed.

Despite these concerns, a recent 5-year Treasury auction was successful, indicating strong foreign demand and overall market confidence in U.S. government bonds.

Stock Market Trends

The stock market overall maintains a positive outlook despite concerns over potential short-term overheating. Julian Emanuel from Evercore ISI warned that the market might be entering an overheated territory, comparing the current situation to the dotcom bubble of 2000. Despite these warnings, expectations of Federal Reserve rate cuts and political developments provide a bullish backdrop for the market.

Market Outlook

Despite potential short-term liquidity pressures due to tax season and the conclusion of the Bank Term Funding Program (BTFP), the Federal Reserve’s anticipated announcement on slowing the pace of quantitative tightening (QT) suggests that any market corrections could represent buying opportunities.

Ed Yardeni from Yardeni Research expresses concern over the rapid market rise but maintains that the bull market is still in its early stages. He notes that the S&P 500 index has recovered all its losses from the previous bear market as of January 19, and historically, rallies have lasted between 132 to 3,894 days after such recoveries, with an average duration of 1,228 days. This suggests that, despite potential corrections, the long-term upward trend is likely to continue.

Furthermore, April historically presents a favorable month for the stock market, according to research from the Carson Group. Since 1950, April has been the second-best month in terms of returns, performing strongly over the last 20 and 10 years, and even in election years. Despite the market having risen for five consecutive months, historical statistics indicate there’s room for further gains. Since 1950, there have been 28 instances of the market rising for five consecutive months, and in the following month, the market continued to rise 75.9% of the time, with a 92.9% chance of rising over the subsequent 12 months. This underscores that adjustments are often temporary, with the long-term trend favoring growth.

Federated Hermes’ Analysis: Embracing “Goldilocks Plus”

Federated Hermes has dubbed the current market condition as “Goldilocks Plus,” highlighting five main reasons for their optimistic outlook:

1. Robust Economic Fundamentals: Ongoing economic recovery is evidenced by improving leading economic indicators, a strong labor market, and rising manufacturing PMI. Consumer spending remains solid due to employment and wage growth.

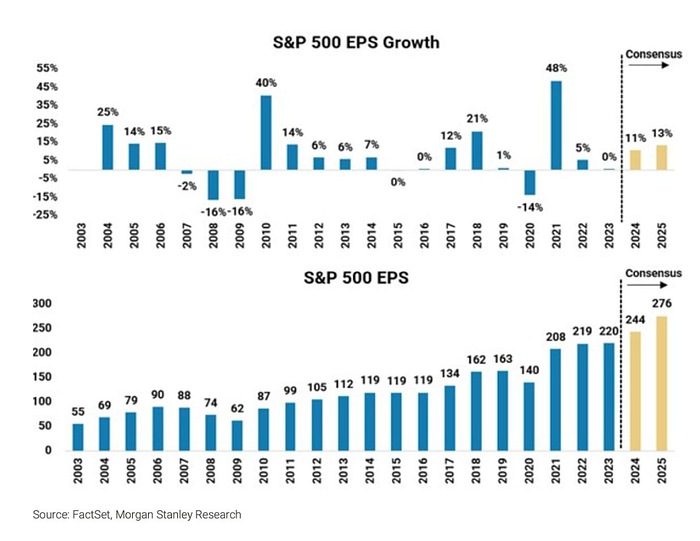

2. Accelerating Corporate Earnings: S&P 500 companies have reported earnings growth exceeding expectations, with projections of further acceleration in the latter half of the year. Sectors beyond technology, including healthcare, finance, and materials, are expected to join this upward trend.

3. A Shift in the Fed’s Stance: Despite recent inflation upticks, Fed Chair Powell’s dovish posture at the latest FOMC meeting surprised many. While Fed anticipates three rate cuts this year, a strong economy and sticky inflation suggest potentially fewer cuts, which could still buoy the market.

4. Political Environment Becoming More Favorable: As the presidential election approaches, market volatility expected by some may give way to policies favoring deregulation, growth-oriented tax cuts, and more controlled border policies, regardless of the election outcome.

5. Reasonable Market Prices: Despite the optimistic outlook, the broader market, excluding the ‘Magnificent 7’ stocks, trades at a reasonable price-earnings ratio, with certain sectors like the Russell 2000 Value Index appearing even more attractively priced.

Federated Hermes maintains an “overweight” stance on stocks, focusing beyond the ‘Magnificent 7’ and advising investors to consider buying on dips rather than selling during rallies. Holding a firm grip on stocks is recommended, echoing the sentiment that in a bull market, it’s advisable to buy on declines rather than sell on rallies, emphasizing the confidence in long-term market resilience.

The Baltimore Port Bridge Collapse

A significant incident occurred early today at the Baltimore port when the ‘Francis Scott Key Bridge’ collapsed following a collision with a large container ship. This bridge plays a crucial role in handling 15% of the U.S.’s import and export volume. The 2.6 km long bridge’s collapse has halted ship traffic to the port, potentially impacting automobile and parts import and export significantly. Ford’s CFO, John Lawler, commented on the potential disruptions to the flow of goods through this major port, though the overall impact on the U.S. supply chain remains uncertain.